{kind=link}

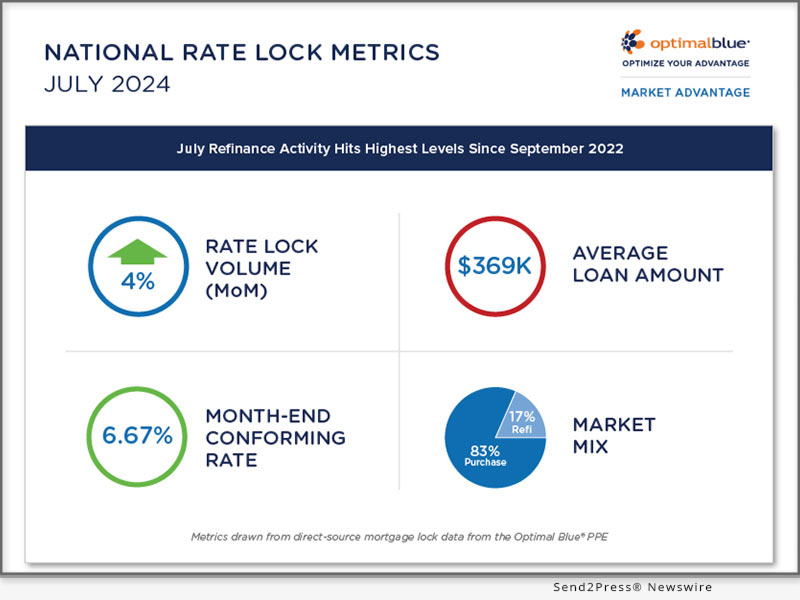

Optimal Blue today released its July 2024 Market Advantage mortgage data report, which revealed that mortgage refinance demand surged to levels not seen since September 2022 amid softening interest rates. The lower interest rates seen in July also coaxed increased purchase activity, which, combined with greater refi activity, drove a 3.5% month-over-month (MoM) increase in mortgage rate lock volumes.

Optimal Blue’s July 2024 Market Advantage mortgage data report shows a lift in mortgage activity amid softening interest rates

PLANO, Texas /Mortgage and Finance News/ — Optimal Blue today released its July 2024 Market Advantage mortgage data report, which revealed that mortgage refinance demand surged to levels not seen since September 2022 amid softening interest rates. The lower interest rates seen in July also coaxed increased purchase activity, which, combined with greater refi activity, drove a 3.5% month-over-month (MoM) increase in mortgage rate lock volumes.

“The July report shows a notable uptick in refinance activity, particularly rate-and-term refinances, which jumped 12% as borrowers responded to declining interest rates,” said Brennan O’Connell, director of data solutions at Optimal Blue. “The drop in the Optimal Blue Mortgage Market Indices 30-year conforming rate to 6.67% played a significant role in this growth, and we observed the highest level of refinance activity since September 2022.”

Key findings from the Market Advantage report, which are drawn from direct-source mortgage lock data, are:

* Increase in rate lock volume: Overall rate lock volume rose by 3.5% MoM, with purchase activity up 2.5% and refinance activity showing even stronger growth. Cash-out refinance volume grew by 5.9% MoM, while rate-and-term refinance activity surged 12.3%, reflecting borrower sensitivity to lower rates.

* Purchase lock count growth: Purchase lock counts grew by 2.5% MoM in July, though they remained down 7% year-over-year (YoY). This is a significant improvement over June’s 17% YoY decline, suggesting a potential stabilization in purchase demand as the market adjusts.

* Refinance activity surge: Refinance activity reached its highest level since September 2022, with the refinance share growing to 17% of total volume – an 81-basis-point increase from June and a 472-basis-point rise YoY. This aligns with trends in the OBMMI 30-year conforming rate, which ended July 2024 at 6.67%, nearly identical to the 6.68% rate that closed out September in 2022.

* Rate and treasury movements: The OBMMI 30-year conforming rate ended July at 6.67%, down 26 basis points from June. Meanwhile, the 10-year Treasury yield dropped by 27 basis points to 4.09%. The spread between the 30-year conforming rate and the 10-year Treasury remained stable at 258 basis points, an uptick of just 1 basis point.

* Shift in loan mix: The loan mix in July shifted toward agency production. Conforming loans increased market share to 56.1% (+18 bps), FHA loans grew to 19.0% (+61 bps), and VA loans rose to 11.9% (+22 bps). Conversely, non-conforming loans, including jumbo and non-QM, saw a decline in market share, falling to 12.4% (-107 bps).

* Decrease in average loan amount: The average loan amount decreased from $374K in June to $369K in July, reflecting the shift away from non-conforming loan types.

* Stable credit quality: Credit scores remained stable, with the average score holding steady at 732.

The full July 2024 Market Advantage report provides more detailed findings and additional insights into U.S. mortgage market trends (PDF): https://www2.optimalblue.com/wp-content/uploads/2024/08/OB_MarketAdvantage_MortgageDataReport_July2024.pdf.

About the Market Advantage Report:

Formerly known as the Originations Market Monitor, Optimal Blue issues the Market Advantage mortgage data report each month to provide early insight into U.S. mortgage trends. Leveraging lender rate lock data from the Optimal Blue PPE – the mortgage industry’s most widely used product, pricing, and eligibility engine – the Market Advantage provides a view of early-stage origination activity. Unlike self-reported survey data, mortgage lock data is direct-source data that accurately reflects the in-process loans in lenders’ pipelines.

Nothing herein shall be construed as, nor is Optimal Blue providing, any legal, trading, hedging, or financial advice.

About Optimal Blue

Optimal Blue effectively bridges the primary and secondary mortgage markets to deliver the industry’s only end-to-end capital markets platform. The company helps lenders of all sizes and scopes maximize profitability and operate efficiently so they can help American borrowers achieve the dream of homeownership. Through innovative technology, a network of interconnectivity, rich data insights, and expertise gathered over more than 20 years, Optimal Blue is an experienced partner that, in any market environment, allows lenders to optimize their advantage from pricing accuracy to margin protection, and every step in between. To learn more, visit https://OptimalBlue.com/.

Learn More: https://www2.optimalblue.com/

This version of news story was published on and is Copr. © 2024 Mortgage & Finance News™ (MortgageAndFinanceNews.com) – part of the Neotrope® News Network, USA – all rights reserved.

Information is believed accurate but is not guaranteed. For questions about the above news, contact the company/org/person noted in the text and NOT this website.

STORY ID: S2P120237 NEOMORTGFIN