{kind=link}

Sales Boomerang, the mortgage industry’s top-rated automated borrower intelligence and retention system, today released its latest Mortgage Market Opportunities Report. The Q4 2021 report identified increasing opportunities for mortgage lenders to assist borrowers with tappable home equity, lending credence to analysts’ expectations for a surge in home-equity-related mortgage activity in 2022.

Home-equity gains signal a shift in the kinds of opportunities that will dominate lenders’ pipelines in 2022

WASHINGTON, D.C. /Mortgage and Finance News/ — Sales Boomerang, the mortgage industry’s top-rated automated borrower intelligence and retention system, today released its latest Mortgage Market Opportunities Report. The Q4 2021 report identified increasing opportunities for mortgage lenders to assist borrowers with tappable home equity, lending credence to analysts’ expectations for a surge in home-equity-related mortgage activity in 2022.

Methodology

The Mortgage Market Opportunities Report draws on Sales Boomerang system data to identify market opportunities of relevance to today’s borrowers and lenders. To generate the report, Sales Boomerang reviewed data from more than 160 residential mortgage lenders that use its borrower intelligence and retention tools to monitor millions of customer and prospect records. Sales Boomerang then calculated and compared the aggregate frequency with which those contact records triggered loan-opportunity, prescriptive-scenario and risk-and-retention alerts during the third and fourth quarters of 2021.

Key Findings*

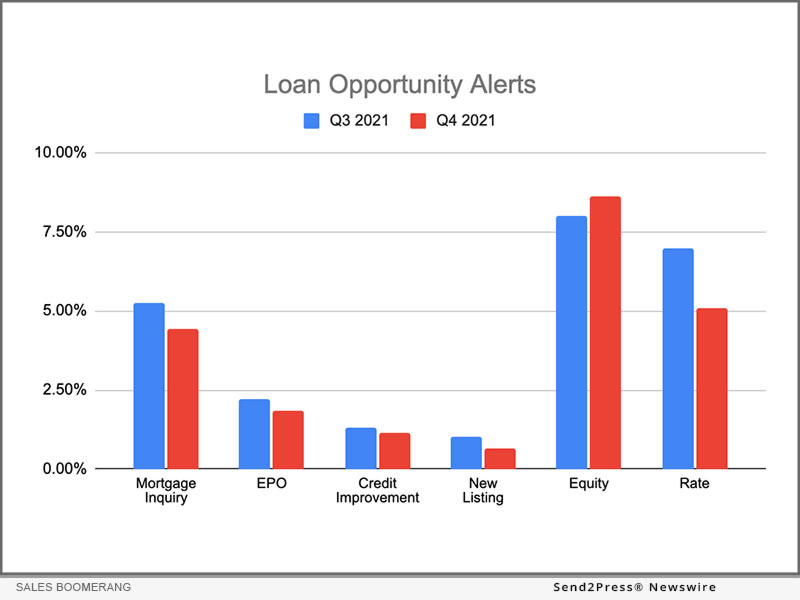

Sales Boomerang’s loan-opportunity alerts identify the contacts inside a lender’s database who are actively shopping for a mortgage loan or who may be able to benefit from a new mortgage loan. Across the sample group, the frequency of each alert type in Q4 2021 was as follows:

* Mortgage Inquiry Alert: 4.42% of monitored contacts (down 16.13% from Q3)

A customer or prospect has shopped with a competitor in the last 24 hours.

* EPO Alert: 1.84% of monitored contacts (down 17.49% from Q3)

A customer or prospect whose loan closed ≤ 6 months ago has shopped with a competitor in the last 24 hours.

* Credit Improvement Alert: 1.14% of monitored contacts (down 13.64% from Q3)

A customer or prospect has improved their FICO score.

* New Listing Alert: 0.64% of monitored contacts (down 38.46% from Q3)

A customer or prospect has listed their home for sale.

* Equity Alert: 8.61% of monitored contacts (up 7.36% from Q3)

A customer or prospect’s home equity has increased.

* Rate Alert: 5.07% of monitored contacts (down 27.16% from Q3)

The interest rate of a customer or prospect’s existing mortgage is significantly higher than current prevailing rates.

Sales Boomerang’s prescriptive-scenario alerts analyze not only whether a consumer could benefit from a given loan type, but also whether the consumer is credit-qualified to apply for financing. This additional layer of intelligence makes prescriptive-scenario alerts among the highest-converting available to mortgage lenders today. The frequency of each alert during Q4 2021 was as follows:

* Cash-Out Alert: 5.08% of monitored contacts (up 17.87% from Q3)

A borrower is credit qualified and has built sufficient equity to tap into the cash in their home.

* Rate-and-Term Alert: 10.05% of monitored contacts (up 160.36% from Q3)

A borrower is credit qualified and can benefit from the current interest rates for a refinance.

* Debt Alert: 1.33% of monitored contacts (down 23.12% from Q3)

A borrower is credit qualified and can benefit from paying off other debts with the equity in their home.

* FHA MI Removal Alert: 14.01% of monitored contacts (up 92.71% from Q3)

An FHA borrower has exceeded 20% equity and can remove mortgage insurance (MI).

For a subset of lenders that maintain servicing portfolios, the frequency of risk-and-retention alerts was as follows:

* Risk & Retention Alert: 31.18% of monitored contacts (down 13.82% from Q3)

A customer is engaging in one or more of 15 credit activities that may put their serviced loan at risk

Analysis*

* When a borrower puts less than 20% down on an FHA-insured loan, they are required to pay mortgage insurance (MI) premiums on top of their monthly principal and interest payments. FHA borrowers with MI may be unaware they have the option to remove their MI once they reach 20% equity. With a nearly 93% quarter-over-quarter increase in FHA MI Removal alerts, lenders have the opportunity to deliver immediate monthly savings to borrowers.

* Since Sales Boomerang’s Cash-Out alerts only trigger for credit-qualified contacts, continued gains in this alert category show that borrowers are growing their credit scores alongside their equity. Lenders should prepare for continued cash-out refinance and HELOC activity in the coming months.

* Keen observers will notice that the Rate and Rate-and-Term alerts trended in opposite directions from Q3 to Q4. Following a year of interest rate growth, fewer consumers are positioned to benefit from a refinance solely based on the difference between their current interest rate and prevailing market rates – thus, the decline in Rate alerts. But a higher frequency of Rate-and-Term alerts indicates that even if the overall refi market is down, there’s a growing subset of consumers who have the home equity and credit profiles necessary to benefit from a refinance.

* Mortgage Inquiry and EPO alerts declined for a third consecutive quarter, and New Listings were down for a second quarter in a row. With fewer consumers actively putting themselves in the market for mortgage products, lenders will need to be proactive in bringing financially advantageous opportunities to potential customers.

* Q4’s 14% drop in Risk & Retention alerts was the category’s first significant decline in 2021. Nonetheless, with nearly one in three borrowers still exhibiting risky credit behaviors, mortgage servicers should keep a close eye on their portfolios for default risk.

“Borrowers aren’t always aware of the multitude of ways they can leverage their home equity, yet it’s becoming increasingly clear that equity is creating some of the best financial opportunities for borrowers and lenders today. It is up to us to help mortgage advisors bring these opportunities to the table for their customers,” said Sales Boomerang CEO Alex Kutsishin. “Experts may have predicted 2022 would be a year to focus on purchase transactions, but our data shows lenders would be well-served to shine equal light on home-equity lending.”

*Key findings and analysis provided for informational purposes only. The data represented in the Mortgage Market Opportunities report is historical. Past performance is not a reliable indicator of future results. Sales Boomerang accepts no responsibility or liability for readers’ use of the key findings or analysis included in this report.

About Sales Boomerang:

Sales Boomerang transformed the relationship between mortgage lenders and borrowers with the introduction of the first automated borrower intelligence system in 2017. The company’s intelligent alerts notify lenders as soon as a past customer or prospect is ready and credit-qualified for a loan. As the mortgage industry’s #1 borrower retention tool, Sales Boomerang is trusted by more than 150 lenders – including brokers, independent mortgage companies, credit unions and banks – to help build lasting borrower relationships that maximize lifetime customer value. To date, Sales Boomerang alerts have enabled lenders to close more than $150 billion in additional loan volume that would have otherwise been overlooked and achieve customer retention rates that outperform industry norms by an average of 3-5X. To learn more about Sales Boomerang and its No Borrower Left Behind™ ethos, visit https://www.salesboomerang.com.

Learn More: https://www.salesboomerang.com/

This version of news story was published on and is Copr. © 2022 Mortgage & Finance News™ (MortgageAndFinanceNews.com) – part of the Neotrope® News Network, USA – all rights reserved.

Information is believed accurate but is not guaranteed. For questions about the above news, contact the company/org/person noted in the text and NOT this website.

S2P STORY ID: 78541